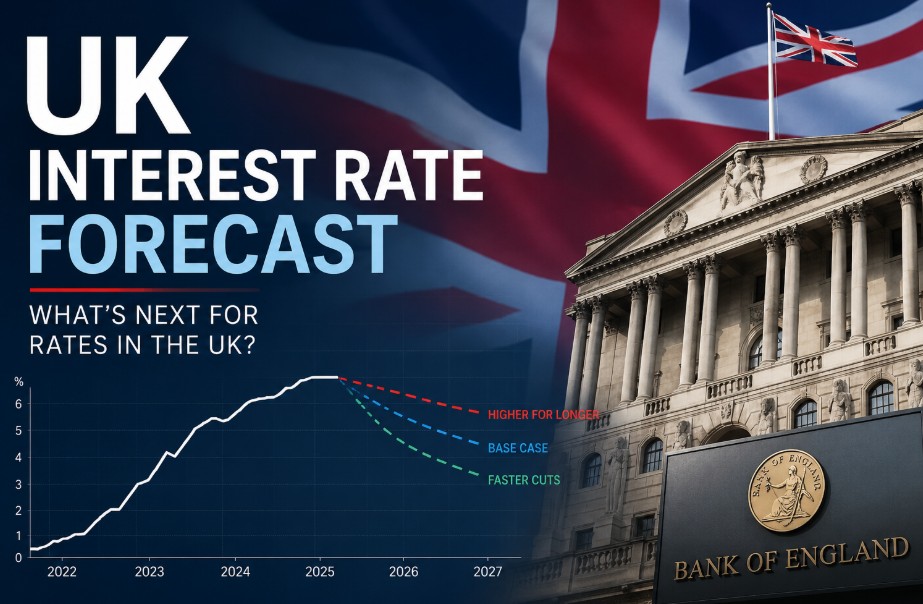

The primary UK interest rate forecast indicates that the Bank of England base rate will remain held at 3.75% during the mid-2026 sessions, with a strong probability of staying at this baseline throughout the summer.

While earlier economic projections pointed toward gradual cuts, a recent global energy supply shock caused by escalating geopolitical tensions in the Middle East has forced policymakers to adopt a highly defensive strategy.

Consequently, monetary policy faces a dual-risk trajectory where a temporary rate hike to 4.00% cannot be ruled out if inflation trends upward.

What is the Current UK Interest Rate Forecast for 2026?

The current UK interest rate forecast for mid-2026 places the Bank of England base rate at 3.75%.

Despite earlier expectations of easing, persistent global energy supply shocks and rising geopolitical tensions have forced the committee to maintain a defensive stance, with a temporary hike to 4.00% remaining a distinct possibility.

The Monetary Policy Committee’s current bias is driven by three core factors: headline CPI inflation at 3.3%, core services inflation at 4.8%, and a persistently tight labor market.

These variables restrict the committee’s ability to lower borrowing costs in the immediate term. The primary economic indicators driving this cautious bias include:

| Economic Indicator | Q2 2026 Value | Target / Baseline | Policy Implication |

| BoE Base Rate | 3.75% | 4.25% (20-Yr Average) | Steady hold with upward risks |

| CPI Inflation Rate | 3.3% | 2.0% Official Target | Restricts scope for near-term cuts |

| Core Services Inflation | 4.8% | 3.0% Structural Baseline | Main driver of hawkish committee bias |

| UK Unemployment Rate | 4.2% | 4.5% Equilibrium Level | Tight labor market supports wage growth |

What Can We Expect From the Next Bank of England Interest Rate Decision?

All eyes are on the upcoming central bank session scheduled for 18 June 2026. The baseline rate is widely expected to be maintained at 3.75%, but the decision-making process is highly data-sensitive and operates strictly on a meeting-by-meeting basis.

The countdown to the official announcement involves a tight sequence of data releases and market monitoring:

- Labor Market Data Release: The Office for National Statistics (ONS) releases the latest monthly labor market data and wage growth statistics, which policymakers scrutinize for domestic inflation signs.

- Swap Rate Monitoring: High-street lenders actively monitor 2-year and 5-year sterling swap rates to adjust their consumer pricing models ahead of the decision.

- CPI Data Print: The MPC receives the crucial, updated Consumer Price Index (CPI) data print to assess the immediate trajectory of inflation.

- Internal Policy Debates: Committee members hold final internal debates, weighing domestic pressures against international energy price shocks and rising import costs.

- Official Rate Announcement: The official Bank Rate decision is announced to the public alongside the formal meeting minutes, revealing the committee’s voting split.

- High-Street Bank Calibration: High-street banks immediately review the central bank’s summary to adjust their Standard Variable Rates (SVR) and commercial credit lines.

How Will UK Interest Rates Evolve in 2027?

The medium-term outlook depends heavily on whether supply chain bottlenecks clear and if domestic consumer demand remains resilient. Economists are mapping out three potential pathways for 2027:

- The Stagnant Baseline Scenario: The base rate remains stuck between 3.50% and 3.75% deep into 2027 due to persistent global structural fragmentation.

- The Delayed Easing Scenario: If inflation successfully drops back to the 2.0% target by spring 2027, the BoE could implement two successive 25-basis-point cuts, lowering the rate to 3.25%.

- The Stagflationary Risk Scenario: In a worst-case outlook involving increased trade barriers and rising energy prices, borrowing costs could be forced up to 4.50% to protect the value of sterling.

What is the Bank of England Interest Rate Forecast for the Next 5 to 10 Years?

Looking beyond immediate business cycles, macroeconomic forecasters agree that the UK has entered a higher-for-longer structural era. A return to the zero-percent rates seen after the 2008 financial crisis is highly unlikely.

This long-term shift is driven by structural forces: deglobalization, supply chain near-shoring, massive capital demands for green energy investments, and heavy public sector net debt.

The timeline below outlines the projected normalization path over the next decade:

| Decade Timeline | Projected Base Rate Range | Primary Economic Growth Drivers | Expected Impact on Assets |

|

(2026 – 2028) Macroeconomic Adjustment & Supply Rebuilding |

3.50% – 4.00% | Energy transition costs, intense supply chain rebuilding | Highly volatile fixed-rate mortgage market |

|

(2029 – 2031) Digital Automation & Stabilization |

3.00% – 3.50% | Digital transformation, widespread automated labor adoption | Stabilization of commercial real estate |

|

(2032 – 2036) Demographic Stabilization & Terminal Rate Alignment |

2.75% – 3.25% | Demographic aging, shifting public spending | Growth in long-term fixed income assets |

Influenced by an aging demographic and shifting public spending. The base rate finally settles into its long-term structural terminal rate, driving growth in long-term fixed income assets.

What is the UK Mortgage Interest Rate Forecast for Homeowners?

The pricing of residential mortgage products remains somewhat disconnected from short-term base rate fluctuations, tracking long-term swap markets instead.

Because 2-year and 5-year swap rates have risen due to Middle East stability risks, standard 5% deposit mortgage rates are expected to stay sticky between 4.85% and 5.40% for the rest of the year.

The prospect of fixed deals dropping below the 4% barrier has largely vanished for the foreseeable future. As volatility persists, borrowers are closely monitoring how major lenders respond to these shifting swap rates.

For instance, recent Barclays NatWest Mortgage Rate Cuts highlight the competitive tension high-street banks face as they attempt to balance profit margins with the need to attract new customers in a high-interest environment.

For a typical family in southern England with a £250,000 variable mortgage, every upward pricing adjustment by high-street lenders adds roughly £45 in monthly interest costs.

Borrowers coming off historical fixed rates face a significant financial adjustment and must choose between the short-term flexibility of a 2-year fix or the long-term inflationary protection of a 5-year lock-in.

What is the UK Savings Interest Rate Forecast for Depositors?

While borrowers face higher costs, cash depositors are enjoying the strongest returns seen in over fifteen years. Capitalizing on this landscape requires a strategic approach to different account types:

- Fixed-Term Yields: Savers can currently lock in guaranteed returns between 4.25% and 4.60% by utilizing multi-year fixed bonds before high-street institutions gradually trim their rates.

- Easy-Access Accounts: Variable savings products will react rapidly to central bank policy, likely dropping toward 3.50% if the base rate is trimmed later next year.

- Tax Efficiency: Maximizing Cash ISA allowances remains an absolute priority to shield interest from taxation, especially as 3.3% inflation continues to erode real post-tax returns.

Summary

The UK economy has entered a structural phase characterized by higher borrowing costs and persistent inflation risks.

With the Bank of England base rate holding at 3.75% ahead of the June review, both households and business operators must adapt to a higher-for-longer landscape.

A reliable UK interest rate forecast means managing debt, protecting profit margins, and optimizing cash reserves for target audiences in 2026.

FAQ about UK interest rate forecast

Will interest rates go down significantly in late 2026?

No, significant rate reductions are highly unlikely this year. Given that CPI inflation has risen to 3.3% amid geopolitical energy disruptions, the central bank will maintain a cautious approach, likely keeping the base rate near 3.75%.

What happens to my mortgage if the Bank Rate stays at 3.75%?

If the base rate holds steady, tracker and variable-rate mortgages will see no immediate change in monthly payments. However, new fixed-rate products will remain exposed to volatility driven by long-term swap market trends.

What is a good interest rate in the UK historically?

In a historical context, a base rate between 3.50% and 4.50% is considered normal. The zero-percent borrowing costs observed after the 2008 financial crisis were an exception, rather than a permanent standard for the economy.

How many interest rate cuts are expected in 2026?

Market expectations have shifted from predicting three rate cuts down to a single reduction, or potentially none at all. Future policy changes depend entirely on service-sector wage data and international supply chain stability.

Should I fix my mortgage for 2 or 5 years in the UK?

Choosing a fixed term depends on your personal need for budget certainty. A 2-year fix provides flexibility to remortgage sooner if macro conditions improve, while a 5-year fix protects against prolonged inflationary pressure.

Why did interest rates stop falling after the cuts in late 2025?

The downward trend paused due to external inflation shocks, specifically rising energy and shipping costs from the Middle East. These factors raised concerns that inflation could become entrenched above the 2% target.

Where will UK interest rates be in 2030?

Long-term structural forecasts suggest that the base rate will settle between 3.00% and 3.25% by 2030. This structural shift is driven by global supply chain re-shoring, energy transition funding, and public sector debt requirements.