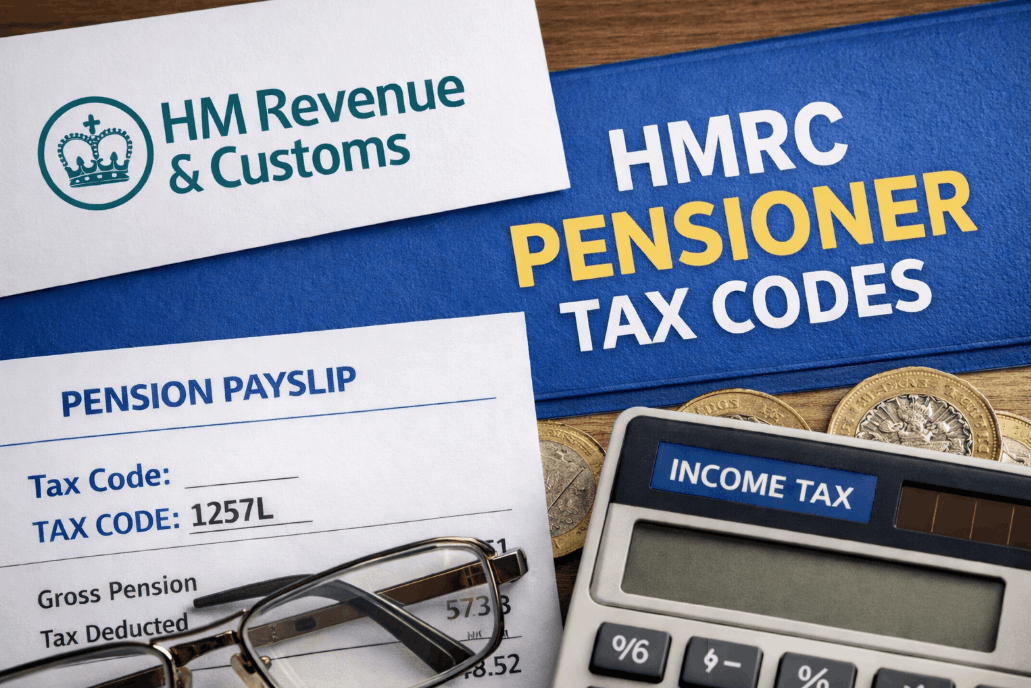

HMRC pensioner tax codes determine how much Income Tax is deducted from your private pensions, annuities, and wages before the money reaches your bank account. In the 2026/27 tax year, most retirees are assigned the 1257L code, representing the frozen £12,570 Personal Allowance.

However, as the State Pension is taxable but paid gross, HMRC often adjusts these codes on secondary income sources to collect the tax due, which can lead to complex K codes or emergency tax implications for those with multiple income streams.

What tax code should a pensioner have?

A standard pensioner in the UK with a single source of income and no significant unpaid tax should typically have the 1257L tax code. This code signals to pension providers that the individual is entitled to the full £12,570 Personal Allowance, meaning the first £1,047 of monthly income is tax-free.

If you have multiple pensions, this allowance is usually applied to the largest pot, while others may be taxed at a flat rate, such as BR (20%) or D0 (40%).

The 2026/27 Standard Threshold

The 1257L code remains the baseline for the current year. The 1257 represents the £12,570 allowance, and the L indicates you are entitled to the standard personal tax-free threshold. A frequent source of complexity arises when this code is divided between two different providers.

For example, if you have a part-time job and a private pension, HMRC may allocate £6,000 of your allowance to the job and £6,570 to the pension. If this split doesn’t match your actual earnings, you may end up overpaying tax throughout the year.

Why is HMRC to rectify tax code issue affecting 11 million pensioners?

HMRC has initiated a large-scale project to rectify tax code inaccuracies caused by fiscal drag and the automation of Simple Assessments.

With the Personal Allowance frozen at £12,570 until 2028, and the State Pension rising under the Triple Lock, over 11 million pensioners are seeing their codes change as they drift into the tax-paying bracket for the first time.

This transition coincides with more rigorous automated auditing, including the recent HMRC wage raid payroll checks, designed to cross-reference employment data with pension distributions for total accuracy.

Understanding the 2026 Rectification Process

- Automatic Adjustments: HMRC’s systems are now cross-referencing DWP State Pension data more frequently to prevent end-of-year underpayments.

- Simple Assessment Letters: Many are receiving PA302 forms, which replace traditional tax codes for those whose only income is the State Pension and modest savings interest.

- Coding Out Arrears: If you owed tax in the previous year, HMRC may have lowered your current code (e.g., to 1100L) to collect that debt automatically.

Are pensioners going to pay tax on State Pension?

The State Pension is taxable income, but it is paid gross, meaning the Department for Work and Pensions (DWP) does not deduct tax before paying you.

Instead, HMRC collects the tax due on your State Pension by reducing the tax-free allowance of your other income, such as a workplace pension or a part-time salary.

| Income Scenario | How Tax is Collected |

| Only State Pension (Below £12,570) | No tax is due; no tax code is required. |

| State Pension + Private Pension | HMRC reduces the private pension tax code to account for State Pension tax. |

| Only State Pension (Above £12,570) | HMRC issues a Simple Assessment bill at the end of the tax year. |

| State Pension + Employment | Your employer’s PAYE code is adjusted to deduct the tax. |

The Pensioner Tax Code Decoder: What do the letters mean?

Tax code letters tell your pension provider exactly how to treat your income. It is a frequent oversight for retirees to overlook the suffix letter, assuming only the numerical value impacts their take-home pay.

However, the letter indicates your specific residency or marital status, which heavily influences the final deduction.

The Dreaded K Code

The K code is essentially a reverse tax code. It is used when your taxable income that cannot be taxed at source (like the State Pension or a company car benefit) is higher than your total tax-free allowance.

Instead of having an amount of income you can earn tax-free, a K code adds a notional amount to your income to ensure the correct tax is collected.

For instance, a code of K475 means HMRC views you as having £4,750 more income than you actually received from that specific provider to catch up on tax owed elsewhere.

Understanding Suffixes and Prefixes

- BR: Basic Rate. Your entire income from this source is taxed at 20% with no tax-free allowance.

- D0: Higher Rate. Your entire income from this source is taxed at 40%.

- NT: No Tax. This is rare and usually applies to specific exempt incomes or non-residents.

- S or C: If your code starts with S (Scotland) or C (Wales), you are taxed based on the rates set by those respective governments.

How much savings can a pensioner have in the bank in the UK before tax?

In the 2026/27 tax year, most pensioners can have significant savings before paying tax, thanks to the Personal Savings Allowance (PSA). A basic-rate taxpayer can earn £1,000 in interest tax-free, while a higher-rate taxpayer gets a £500 allowance.

Additionally, the Starting Rate for Savings allows those with low earned income to earn up to an extra £5,000 in interest without paying a penny in tax.

Retirees focused on tax-efficient saving may also benefit from initiatives such as HMRC help to save bonus payments, which offer a tax-exempt incentive for those meeting specific low-income criteria.

It is important to monitor these balances as they relate to your overall Personal Savings Allowance (PSA).

What is the HMRC warning for anyone with over 3500 savings in their bank account?

There is no tax on the savings balance itself, but there is a warning regarding the interest generated. With interest rates remaining higher than in previous decades, even a balance of £3,500 in a high-interest account can contribute toward breaching your PSA if combined with other income.

HMRC warns that they now receive automated data from banks; if your interest exceeds your allowance, they will automatically adjust your pensioner tax codes to collect the tax, often without you realizing until your monthly pension drops.

What is the biggest mistake most people make regarding retirement?

Observations from recent 2026/27 tax filings show that the shift from a fixed salary to a flexible drawdown is where most financial leakage occurs. Many retirees treat their pension like a bank account, unaware that the taxman views it as a monthly salary.

Critical Tax Management Errors to Avoid in Retirement

- Taking a large lump sum without checking the Month 1 impact: This triggers an emergency tax that can take months to reclaim.

- Ignoring the Marriage Allowance: If one partner has an income below £12,570, they can transfer £1,260 of their allowance to the other, saving up to £252 per year.

- Failing to notify HMRC of Small Pot lump sums: You can take up to three £10,000 pots under specific rules that don’t affect your Lifetime Allowance or trigger complex coding.

- Forgetting to claim for professional fees or subscriptions: If you still consult or work part-time, these can still be used to reduce your tax code.

- Assuming HMRC knows your Total Income: If you have four different small pensions, HMRC’s systems may guess your primary income incorrectly.

- Neglecting the P60 review: Many pensioners simply file their P60 without checking if the code applied matches their latest HMRC Coding Notice.

- Not using the Personal Tax Account: Relying on the post is slow; the HMRC digital portal is the only way to see real-time code changes.

How do I get an HMRC pensioner tax code refund?

If you have been placed on an emergency tax code or have had too much tax deducted from a lump sum withdrawal, you do not have to wait until the end of the tax year to get your money back. In my experience, using the online portal is significantly faster than the traditional paper route.

7 Steps to Claim Your Tax Refund

- Identify the overpayment: Check your latest pension payslip against your HMRC Coding Notice.

- Choose the correct form: Use P55 if you took a partial sum, P53Z if you emptied the pot, or P50Z if you have stopped working and have no other income.

- Gather your P45: Your pension provider will issue this after a taxable payment.

- Log into your Personal Tax Account (PTA): This is the most secure and fastest method.

- Submit the Claim a Tax Refund request: Upload your digital documents and details of your total estimated income for the year.

- Verify your bank details: Ensure HMRC has your current BACS info for a direct transfer.

- Monitor the 5-day window: Online claims are typically processed within 5 to 10 working days, whereas postal claims can take 6 weeks.

FAQ about HMRC Pensioner Tax Codes

Why has my tax code changed to K?

A K code means your taxable benefits or State Pension exceed your Personal Allowance. HMRC uses this to add income to your total, ensuring they collect the necessary tax from your remaining private pension or salary payments.

Do I pay tax on my state pension if it’s my only income?

If your State Pension is your only income and it is below £12,570, you pay no tax. If it rises above this threshold (due to the Triple Lock), HMRC will bill you via Simple Assessment.

How much can I have in a savings account before paying tax?

This depends on your total income. If your total income is low, you could earn up to £5,000 in interest tax-free via the Starting Rate for Savings, plus your £1,000 Personal Savings Allowance.

Can I have two different tax codes?

Yes. If you have two pensions, HMRC will often apply a code like 1257L to the largest one and a flat rate code like BR (Basic Rate) to the second one to avoid underpaying tax.

What does 1257L M1 mean?

The M1 (or W1) indicates an emergency Month 1 basis. HMRC calculates your tax only on that specific payment, ignoring any tax you have already paid or allowances you have used earlier in the year.

Is the 1257L tax code for everyone?

No. It is the standard for England and Northern Ireland. If you live in Scotland or Wales, your code will start with S or C, reflecting the different tax bands set by their respective governments.

How long does an HMRC pension tax refund take?

Online claims via the Personal Tax Account are generally settled within 5–10 working days. Postal claims via forms like the P55 usually take between 4 and 6 weeks to be processed.

Summary and Next Steps

Managing your HMRC pensioner tax codes is a continuous task rather than a one-time administrative task. As the State Pension increases and the Personal Allowance remains frozen, the likelihood of coding errors increases.

The most effective starting point is to verify your Estimated Income for the 2026/27 year via the HMRC Personal Tax Account.

If you notice a K or BR code that doesn’t align with your financial reality, taking immediate action is vital to prevent a significant reduction in your monthly take-home pay.

While digital accounts are efficient, many still prefer to resolve the issue through the HMRC telephone number free 0800 0345 opening times, to consult directly with a technician. Ensuring your code is corrected before the next pay cycle can save months of waiting for a refund.