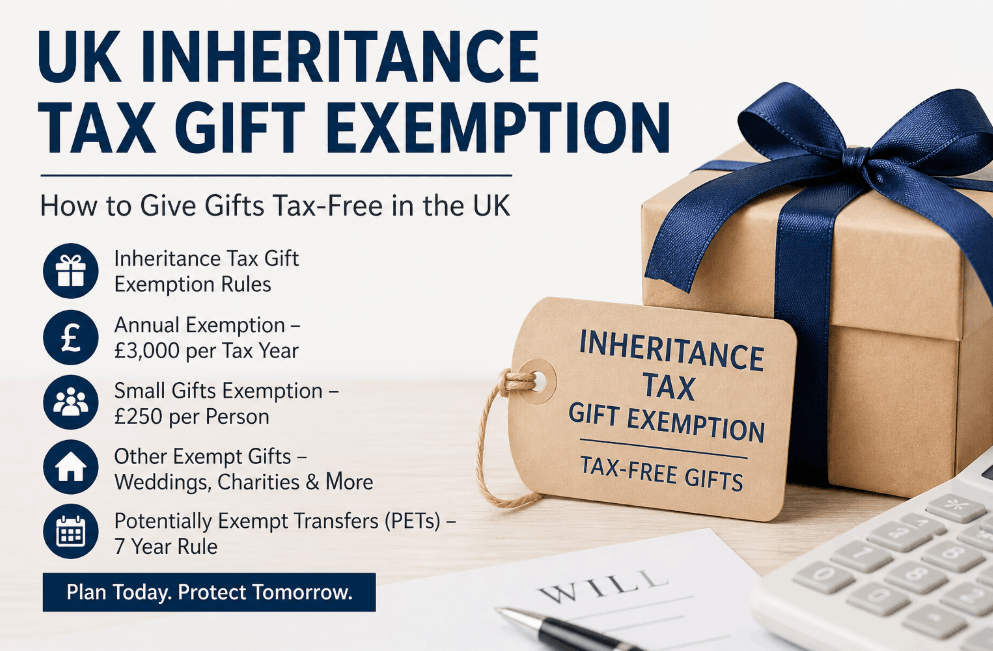

In the United Kingdom, the primary UK inheritance tax gift exemption allows individuals to transfer up to £3,000 per year out of their estate tax-free. Additionally, small gifts up to £250 and regular payments from surplus income remain exempt, provided they do not diminish the donor’s standard of living.

What is the UK inheritance tax gift exemption?

The UK inheritance tax gift exemption is a set of legal provisions that allow individuals to give away money or assets during their lifetime without those gifts being included in the valuation of their estate for tax purposes upon death.

These exemptions are designed to encourage lifetime giving and help families manage the impact of the 40% inheritance tax (IHT) rate.

Effective estate planning requires an understanding of which gifts are immediately exempt and which are potentially exempt.

While the standard Nil-Rate Band remains frozen at £325,000 until 2031, utilizing annual allowances, such as the £3,000 annual exemption and the small gift allowance, remains the most accessible way for UK residents to reduce a future tax bill.

In practice, many families overlook the normal expenditure out of income rule, which has no upper financial limit but requires rigorous record-keeping to satisfy HMRC.

Which gifts are immediately exempt from Inheritance Tax?

When a gift is classified as immediately exempt, it is removed from the donor’s estate the moment it is given. There is no need to survive for seven years for these specific allowances to take effect.

- Annual Exemption: Every individual can give away £3,000 worth of gifts each tax year. If unused, this can be carried forward for exactly one year, allowing a maximum exemption of £6,000.

- Small Gift Allowance: You can give up to £250 to as many people as you want, provided they have not received any part of your £3,000 annual exemption.

- Wedding Gifts: Parents can gift £5,000, grandparents £2,500, and others £1,000 to a couple getting married or entering a civil partnership.

- Spousal Transfers: Gifts between UK-domiciled spouses or civil partners are unlimited and completely tax-free.

Summary of Fixed Gifting Allowances (2026/27)

| Allowance Type | Amount (Per Donor) | Frequency |

| Annual Exemption | £3,000 | Annually (Can carry forward 1 year) |

| Small Gift Allowance | £250 | Per Recipient, Annually |

| Wedding Gift (Child) | £5,000 | Per Marriage |

| Wedding Gift (Grandchild) | £2,500 | Per Marriage |

| Normal Expenditure | Unlimited | Regular (Must be from surplus income) |

How does the Normal Expenditure out of Income exemption work?

This is perhaps the most powerful yet misunderstood UK inheritance tax gift exemption. It allows for unlimited gifting, provided the money comes from your regular monthly income rather than savings or capital.

To qualify, you must demonstrate that the gifts are part of a habitual pattern and that you can maintain your current standard of living after the money has been sent.

A common pattern observed by tax professionals involves grandparents paying for school fees or making regular monthly contributions into a grandchild’s Junior ISA. HMRC recently clarified that income for this purpose follows accountancy rules rather than strict income tax definitions.

For example, if an individual receives a pension of £5,000 a month but only spends £3,000 on living costs, the surplus £2,000 can be gifted monthly with immediate IHT exemption.

Understanding the mechanics of your withdrawals is vital, and learning how to avoid paying tax on your pension can further maximize the surplus funds you have available to pass on to loved ones.

Checklist for Documenting Surplus Income Gifts

- Identify Surplus: Calculate your net annual income minus all regular living expenses.

- Establish Regularity: Set up a standing order to prove the habitual nature of the gift.

- Letter of Intent: Write a simple document stating your intention to make these regular gifts from income.

- Keep a Gift Log: Record dates, amounts, and the source of the funds (e.g., September Pension Surplus).

- Maintain Bank Statements: Keep copies of statements showing the income arriving and the gift leaving.

- Review Annually: Ensure your standard of living hasn’t dropped, requiring you to dip into capital.

What is the 7-year rule for Potentially Exempt Transfers?

If a gift does not fall into one of the immediate exemptions listed above, it is known as a Potentially Exempt Transfer (PET).

These gifts only become fully tax-free if the donor lives for at least seven years after the date of the gift. If the donor passes away within this window, the gift is added back into the estate value.

The Taper Relief Mechanism

Many people mistakenly believe that taper relief reduces the value of the gift itself. In reality, it reduces the tax rate applied to the gift, and it only applies if the total value of all gifts made in the seven years prior to death exceeds the £325,000 Nil-Rate Band.

| Years between gift and death | Tax Rate on the Gift |

| 0 to 3 years | 40% |

| 3 to 4 years | 32% |

| 4 to 5 years | 24% |

| 5 to 6 years | 16% |

| 6 to 7 years | 8% |

| 7 or more years | 0% |

Major Changes in 2026: Agricultural and Business Property Relief

Starting April 6, 2026, the landscape for family-run businesses and farms changes significantly. Previously, Agricultural Property Relief (APR) and Business Property Relief (BPR) often provided 100% protection from inheritance tax for these assets.

Under the new 2026 rules, a combined £2.5 million allowance for 100% relief has been introduced. Any value exceeding this £2.5 million cap will only receive 50% relief, resulting in an effective tax rate of 20% on the excess.

This change makes lifetime gifting of business shares even more critical for larger estates. These updates coincide with broader Rachel Reeves inheritance tax changes that aim to reshape how wealth is transferred across generations in the UK.

For instance, a family farm valued at £4 million would now face a tax charge on the portion above the combined allowances, whereas previously it might have passed entirely tax-free.

Why April 2027 changes your gifting strategy?

The 2027 reform is perhaps the most significant shift in recent estate planning history. From April 6, 2027, unused pension funds and death benefits will be included in the value of an individual’s estate for inheritance tax purposes.

Staying informed about these pension savings inheritance tax changes is crucial for anyone who has previously viewed their retirement pot as a primary vehicle for tax-free legacy planning.

Historically, pensions were the last port of call for spending because they sat outside the IHT net.

With the 2027 change, the strategy reverses: it may now be more tax-efficient to spend pension wealth during your lifetime while gifting other assets, like cash or property, to take advantage of current gift exemptions and the 7-year rule.

How to manage your inheritance tax gift records?

When reviewing decisions made by executors, HMRC often requests proof of gifting history. Without a paper trail, gifts that should have been exempt may be taxed at 40%.

7 Steps to Perfect Gift Record Keeping

- Use a Dedicated Folder: Store all gift-related documents in one physical or digital place.

- Note the Recipient: Clearly state who received the gift and their relationship to you.

- Record the Exact Date: The 7-year clock starts on the day the transfer is completed.

- Specify the Asset: Note if it was cash, property, or shares (including the valuation at the time).

- Identify the Exemption: Mark if you are claiming the £3,000 annual allowance or surplus income.

- Store HMRC Forms: If you have made a Chargeable Lifetime Transfer (e.g., into a trust), keep the IHT100 forms.

- Tell Your Executors: Ensure the person managing your will knows where these records are kept to avoid a lengthy probate audit.

Final Summary

Planning for inheritance tax in 2026 and beyond requires a proactive approach to gifting. By maximizing immediate exemptions, particularly the £3,000 annual allowance and the surplus income rule, donors can significantly reduce their taxable estate.

With the 2026 BPR/APR caps and the 2027 inclusion of pensions in IHT, the spend and gift strategy has never been more relevant. The next logical step is to perform a full estate valuation and document your regular income to see how much you can safely move out of your estate today.

FAQ about UK inheritance tax gift exemption

How much can I gift tax-free in the UK 2026?

You can gift £3,000 annually under the annual exemption. You can also give unlimited small gifts of £250 to different people and unlimited regular gifts from surplus income without paying tax.

Does the 7-year rule apply to the £3,000 allowance?

No, the 7-year rule does not apply to the £3,000 annual exemption. This is an absolute exemption, meaning the money is removed from your estate immediately regardless of when you pass away.

What is the gift limit for children’s weddings?

Parents can give £5,000 tax-free for a child’s wedding. This is in addition to your £3,000 annual allowance, meaning you could technically gift £8,000 tax-free in a single year to a child who is marrying.

Can a couple give £6,000 away?

Yes. Because inheritance tax is individual, a married couple or civil partners can each use their £3,000 annual exemption to gift a combined £6,000 per year tax-free.

How does HMRC track gifted money?

HMRC typically reviews bank statements and financial records during the probate process. Executors are legally required to disclose any gifts made by the deceased in the seven years prior to their death.

Is the £250 gift limit per year or per month?

The £250 small gift allowance is per tax year, per recipient. You can give this amount to as many people as you like, as long as they haven’t received other gifts from you.

What happens if I gift more than £325,000?

Gifts exceeding the £325,000 Nil-Rate Band that do not fall under other exemptions are subject to the 7-year rule. If you die within 7 years, the recipient may have to pay tax via taper relief.